- Services

-

-

-

-

Getting started

Getting startedEasy process with an expert tax preparer

-

US expat tax return

US expat tax returnNo matter where you reside — you must file US tax returns

-

Streamlined procedure

Streamlined procedureNo matter where you reside — you must file US tax returns

-

Non-resident tax preparation

Non-resident tax preparationTFX helps non-US aliens or Green Card holders file returns

-

Tax preparation fee calculator

Tax preparation fee calculatorDiscover the average cost of tax return preparation for you

-

Free intro consultation

Free intro consultationGet started call with tax preparer

-

Tax planning

Tax planningHigh-level phone consultations with experts

-

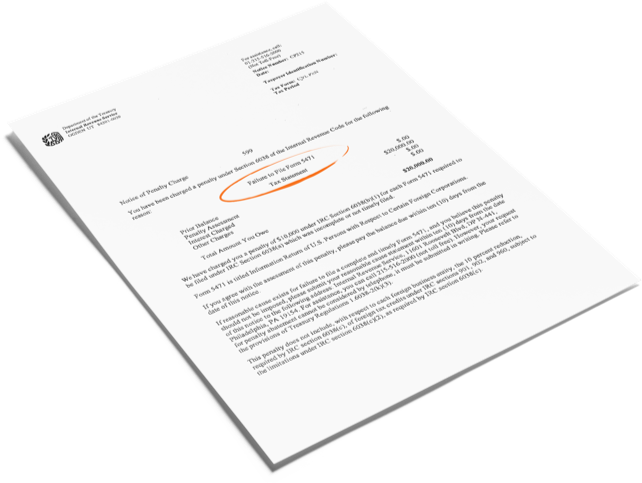

IRS letters review

IRS letters reviewScary letter from the IRS? TFX can help

-

Tax projection

Tax projectionSelling stocks? New job? Make educated financial decisions

- Substantial presence test calc

Easily determine your US tax residency status

-

Core ($450)

Core ($450)Form 1040 federal tax return package

-

Premier ($525)

Premier ($525)For those with additional income sources beyond the core package.

- Streamlined procedure ($1,450)

For those who have not filed and want to become compliant with amnesty from penalties.

-

-

-

-

- Services

-

-

-

- Getting started

Easy process with an expert tax preparer

- US expat tax return

No matter where you reside — you must file US tax returns

- Streamlined procedure

No matter where you reside — you must file US tax returns

- Non-resident tax preparation

TFX helps non-US aliens or Green Card holders file returns

- Tax preparation fee calculator

Discover the average cost of tax return preparation for you

- Free intro consultation

Get started call with tax preparer

- Tax planning

High-level phone consultations with experts

- IRS letters review

Scary letter from the IRS? TFX can help

- Tax projection

Selling stocks? New job? Make educated financial decisions

- Substantial presence test calc

Easily determine your US tax residency status

- Core ($450)

Form 1040 federal tax return package

- Premier ($525)

For those with additional income sources beyond the core package.

- Streamlined procedure ($1,450)

For those who have not filed and want to become compliant with amnesty from penalties.

-

-

-

-